Market Verdict on Iron Ore:

• Neutral to bearish.

Macro

• According to the minutes from U.S. Fed meeting, most officials believed that it was necessary to raise interest rates by 50 basis points once or more times during the year. It may be appropriate to reduce the asset ceiling by $95 billion per month. The upper limit of scale reduction may be implemented gradually within three months.

• The executive meeting of China’s State Council would utilise timely and flexible basket of monetary policy tools, increase support for the real economy, and consider other measures to boost consumption. According to Bloomberg news, Goldman Sachs expected that after the epidemic controlled, China potentially prioritise monetary ease policy and then accelerate infrastructure construction.

Iron Ore Key Indicators:

• Platts62 $158.20, +5.25, MTD $150.50. MACF was still the most popular mid-grade which is more cost-effective to mills. Heavy discount fines and low grade contributed the major trades on seaborne market as well as portside market when major mid-grade like PBF was imported in a wide loss versus portside.

• MySteel 45 ports iron ore arribals at 20.19 million tonnes, up 934,000 tonnes w-o-w. China six northern ports iron ore arrivals at 9.05 million tonnes, up 375,000 tonnes w-o-w.

SGX Iron Ore 62% Futures& Options Open Interest (Apr 6th)

• Futures 79,049,900 tonnes(Increase 1,165,000 tonnes)

• Options 80,483,500 tonnes(Increase 1,165,000 tonnes)

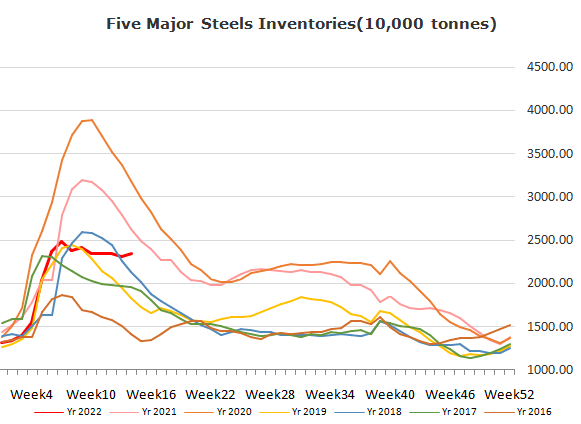

Steel Key Indicators

• China Tangshan area steel mills billet cost after tax at 4684 yuan/tonne, up 103 yuan/tonne. Steel mills gross profit at 196 yuan/tonne, down 53 yuan/tonne w-o-w.

• Russian government expect to raise scrap steel tariff by three times to gurantee the domestic supply and resist the spiking steel price. However the export quota remain unchanged.

Coal Indicators

• The interests of hard coking coal were majorly from ex-China areas. However the Australia FOB coking coal and CFR China coking coal spread has narrowed from $220 to $-97 – a $317 correction on the difference, which mainly caused by speedy growth of Asian prime coking coal alternatives, China demand decrease as well as European major downstream end-users were at a halt.