Market Verdict on Iron Ore:

• Neutral.

Macro

• The U.N. decreased the global economy growth rate at 3.1%, lower than 4% expectation estimated in January. Expected inflation rate at 6.7%, nearly trippled the average inflation level from 2010- 2020, contributed by the massive increase on grains and energy price.

• U.K. CPI up 9% in April, refreshed 40 year high. March CPI up 7%. Eurozone April CPI up 7.4%, created 25 year-high. March CPI 7.5%.

Iron Ore Key Indicators:

• Platts62 $126.60, -3.55, MTD $133.23. Seaborne PBF obtained growing interests, in particular after price correction. However buyers are still preferring MACF. China MACF at port areas decreased fast. South Flank mines expected to ship more MACF to China. 65-62 spread remained narrow around $23 because of the thin steel margin. Some traders indicated that mills resold Carajas fine considering the cost. SSF discount narrowed for consecutive months while SSF/PBF ratio also narrowed, indicating the low grade fines are favorable options for end-users to optimise cost-efficiency.

• Vale indicated that 100 million iron reo capacity was in the process of recovery with starting of multiple new built projects. Vale expect the annual capacity in 2023 would reach 400 million tons.

SGX Iron Ore 62% Futures& Options Open Interest (May 18th)

• Futures 77,135,800 tons(Increase407,700 tons)

• Options 75,259,500 tons(Increase 988,000 tons)

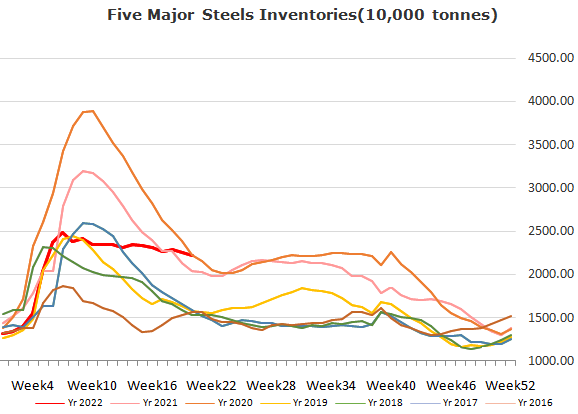

Steel Key Indicators

• Tangshan billet cost 4664 yuan/ton, down 57 yuan/ton w-o-w. Average profit – 144 yuan/ton, down 63 yuan/ton.

Coal Indicators

• The Australia FOB and CFR China disparity had increased by $26 in the current two days. Australia FOB price was supported by the firm bids to chase the June tenders. China saw improved sentiments in Shanxi by significantly increased volume. However China eastern and northern mills were resisting the purchase price on coking coal.