Market Verdict on Iron Ore:

• Neutral.

Macro

• U.S. White House officials were discussing to restrict fuel oil export, to control petroleum price below $5/gallon. Russian PM revealed that Russia would not reduce oil production.

• BOE increased interest rate by 25bp to 1.25%, refreshed the highest since January 2009.

• China NDRC expected CPI would finalised below 3% by the end of 2022, and also expected PPI would fall after the self-reliance of coal and grains increasing.

Iron Ore Key Indicators:

• Platts62 $129.50, -1.35, MTD $140.11. Mainstream iron ores didn’t saw any active buyers during this week although improving import margins. The steel margin was suffering a loss. As expected, iron ore eroded steel mills margin and made an overdraft of growth in advance. Thus, mills are currently utilising premier coking coals to increase reducibility of low grade iron ore, which could reduce cost comprehensively. The 45% tax increase on Indian pellets and previous Ukraine supply disruption to Asian countries led to a global seaborne pellets shortage, which yet to see any alternative.

• MySteel 45 ports iron ore inventories at 126.65 million tons, down 1.8 million tons w-o-w. Daily evacuation 3.06 million tons, down 123,500 tons w-o-w. Australia iron ore 59.12 million tons, down 1.04 million tons w-o-w. Brazil iron ore 42.82 million tons, down 734,500 tons w-o-w. 93 ships at ports, up 8.

SGX Iron Ore 62% Futures& Options Open Interest (Jun 15th)

• Futures 84,336,900 tons(Increase 144,900 tons)

• Options 80,770,500 tons(Increase 942,500 tons)

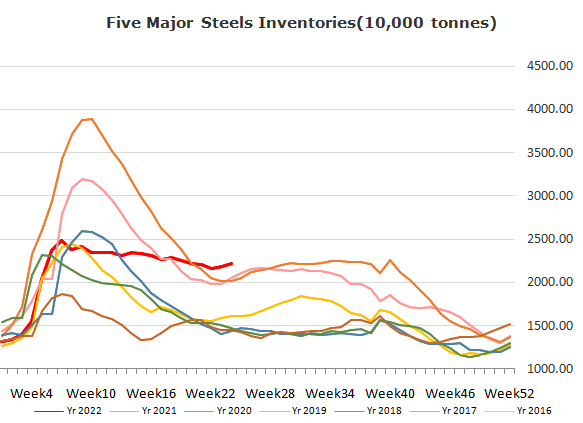

Steel Key Indicators

• 40 independent EAFs construction steel average cost 4798 yuan/ton, down 95 yuan/ton w-o-w. Average loss 143 yuan/ton w-o-w.

Coal Indicators

• After Australia FOB market sharp falling over previous few weeks, buying interests emerged in the market. PLV was stable at $381/mt FOB Australia. China domestic coking coal market continued to strengthen as Shanxi Liulin high sulfur auctions saw 300 yuan/mt than starting price.