Market Verdict on Iron Ore:

• Neutral to bullish.

Macro

• China NBS published July CPI annual rate up 2.7%, expand 0.2% compared with June, refreshed the highest since August 2020. PPI July up 4.2%, narrowed 1.9% compared with June, created consecutive decrease for nine months. Both numbers were lower than expectations.

Iron Ore Key Indicators:

• The term contract discounts for FMG in August widened in August, however market participants indicated that the current discounts were not great enough to attract buying interest. Mainstream seaborne cargoes including PBF, MACF, NMHG and JMBF were traded actively during the past two weeks. However the secondary market maintained quiet, indicating the demand market was yet to catch up with the fast increasing price on primary market.

• Aug 1- 7th MySteel 19 ports iron ore deliveries at 26.11 million tons, down 421,000 tonnes on the week. Australia deliveries at 19.06 million tons, up 1.55 million tons on the week. Brazil deliveries 7.06 million tons, down 1.97 million tons on the week. Global iron ore deliveries at 31.22 million tons, down 11.18 million tons on the week.

SGX Iron Ore 62% Futures& Options Open Interest (Aug 9th)

• Futures 93,394,200 tons(Increase 247,200 tons)

• Options 87,565,500 tons(Increase 405,500 tons)

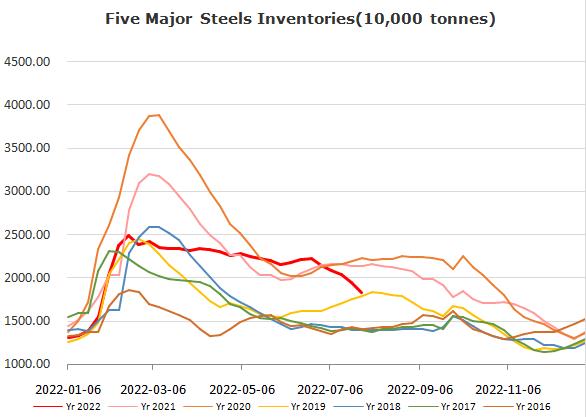

Steel Key Indicators

• China Shagang Group, Zenith and Yonggang Group increased scrap purchase price by 200 yuan/ton, biggest increase in the year.

• BaoSteel plate and HRC price in September decreased by 100 yuan/ton.

Coal Indicators

• The first round of physical coke price rise by 200- 240 yuan will be fully implemented during Aug 9-10th.

• Indonesia punished 29 coal exporters who failed to meet their domestic market obligations(DMO).