Market Verdict on Iron Ore:

• Neutral.

Macro

• U.S. dollar index DXY refreshed new high yesterday at 109, a 20-year-high. Non-dollar currencies experienced fast depreciation in past two weeks.

• China Automobile Associaiton: Jan- Jul auto-making profit 273.94 million yuan, down 14.4% on the year, improved 11.1% from Jan-Jun. The auto-making industry contribute 5.6% of the industries value added amount above designated scale.

Iron Ore Key Indicators:

• Platts62 $101.75, -4.05, MTD $105.31. Both seaborne and portside market saw a cooling down on buying interest during the week. PBF inventories at Shandong reached 5 million tons, which were 5 times bigger than normal inventories level in previous few years. Thus, PBF sellers expected to complete the deal before landing on ports. The trades potentially shift from sellers’ option to buyers side. NMHG regained popularity. Chinese northern ports has over 6 million tons of pellets, which hasn’t no change since June. Thus there is no import demand either from June.

SGX Iron Ore 62% Futures& Options Open Interest (Aug 29th)

• Futures 102,615,600 tons(Increase 100,600 tons)

• Options 101,045,100 tons(Increase 305,000 tons)

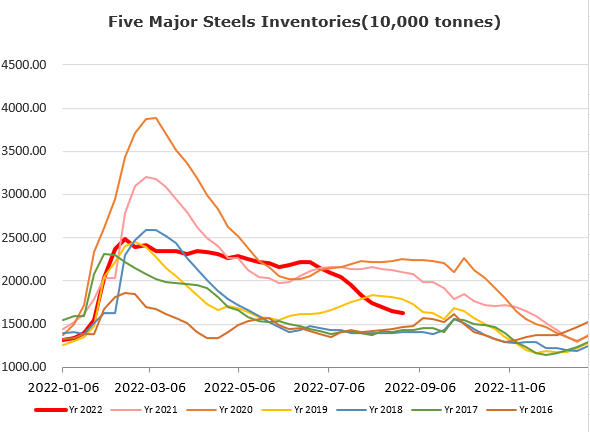

Steel Key Indicators

• H1 Chinese crude steel production 527 million tons, down 6.5% on the year. Pig iron 439 million tons, down 4.7% on the year. CISA member steel mills recognised revenue 334 million yuan, down 4.7% on the year. Member profit 10.34 million yuan, down 55.5% on the year.

Coal Indicators

• Australia met coal saw mixed outlook during the week, since buyers were waiting for new direction. FOB Australia and CFR China PLV index remain flat during the week. India end-users indicated the high coking coal price would stressed their steel margins. China seaborne demand yet to confirm.