Market Verdict on Iron Ore:

• Neutral.

Macro:

• China’s Ministry of Finance: In 2023, China will appropriately increase fiscal expenditure, promote recovery of consumption market.

• U.S. jobless claim increased 9,000 to 225,000, as expected.

• Australia and India signed an agreement ECTA, aiming to decrease the bilateral taxes.

Iron Ore Key Indicators:

• Platts62 $114.75, +0.10, MTD $110.73. With seasonal low stock level at Chinese steel mills, PBF concluded three deals with high float basis at $2.05-2.25/dmt for January laycan, February laycan was traded at float premium at $1.6. Other mid-grade saw significant improvement on float basis prices as well.

SGX Iron Ore 62% Futures& Options Open Interest (Dec 29th)

l Futures 110,561,000 tons(Increase 991,700 tons)

• Options 87,601,300 tons(Increase 948,000 tons)

Steel Key Indicators:

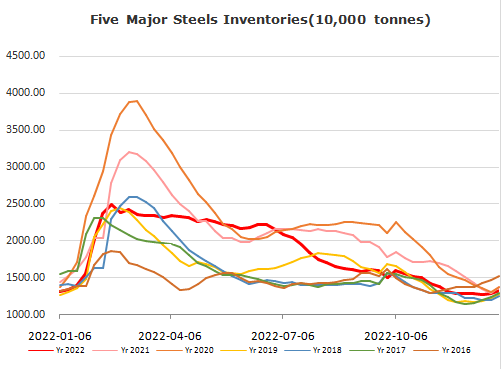

• MySteel researched sample steel mill import iron ore inventories at 95.04 million tons, up 394,900 tons on the week.

• MySteel researched 247 steel mills utilisation rate 75.21%, down 0.72% on the week, up 4.2% on the year. Daily pig iron production at 2.2251 million tosn, up 5,600 on the week, up 195,000 on the year.

Coal Indicators:

• Australia FOB PLV market was flat in early half of the week. The market saw a bid at $285 for Peak Downs HCCLV, for February laycan. Indian end-users indicated that the real market was still at $250-260 level instead of $280-285.

• China Customs Tariff Commission announced to reiterate expiry of zero import duty by March 31, 2023 for met coal and coke imports. The announcement also confirmed import tariffs for varying grades of coal and coke under the category of Most Favored Nation(MFN).