Verdict:

• Short-run Neutral.

Macro:

• The China Macroeconomic Forum (CMF) predicted that the real GDP growth rate in China will rebound to 5% to 5.5% in the fourth quarter in 2023, and the GDP growth rate for the whole year of 2023 will reach 5.1% to 5.3%. Among them, the supply chain recovered, and the three major industries realised significant growth. The demand contraction was improved, prices have been relatively weak, monetary policy has remained loose, and public fiscal revenue has significantly improved.

• China NDRC, Ministry of Market Regulation met with major ports operators on iron ore inventory, storage, loading and unloading charges. The several departments planned to strengthen iron ore supervision at ports and prevent against hoarding iron ores.

Iron Ore Key Indicators:

• Platts62 $135.60, +0.80, MTD $130.25. MACF trade was completed at a discount of $1/dmt based on December Index of IODEX. Import loss on medium grade shift demand to portside again. Most of purchases were demand to spot, while not many pre-stocking of iron ores on the market currently.

SGX Iron Ore 62% Futures& Options Open Interest (Nov 24th)

• Futures 140,207,100 tons(Increase 2,635,700 tons)

• Options 122,713,600 tons(Increase 1,317,500 tons)

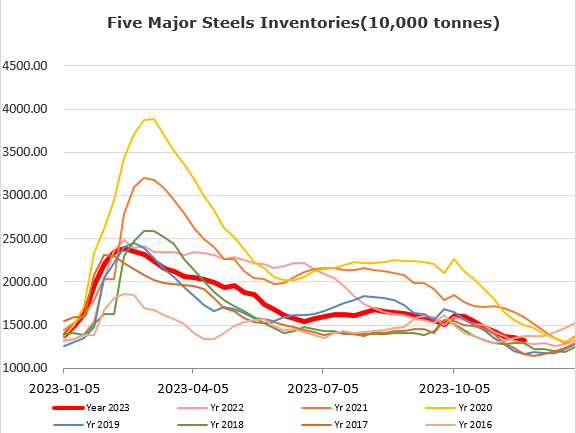

Steel Key Indicators:

• China Tianjin SS400 HRC up $20 to $565, because of the fast appreciation of Chinese yuan and deprecation on USD, which lowered the value of China export steel pricing. In addition, the growth was following to the increase of Europe and Asia steel FOB market.

Coal Indicators:

• China safety supervision teams expected to work in Shanxi province for the coming 6 months. Market started to concern the domestic coking coal supply.