Verdict:

• Short-run Neutral.

Macro:

• BOE’s Broadbent said UK interest rate may drop this summer.

• Chinese builder Vanke took on more loans with 1.2 billion yuan deal.

Iron Ore Key Indicators:

• Platts62 $118.50, +0.50, MTD $117.02. The fast depleting on IOCJ supported the high grade price. In general, MB65- P62 at $15.56 are expected to widen to $17 in June. The recent rebound on ferrous was contributed by the housing stimulus in China and following the growth of gold, silver, and copper. Be aware of the position decrease on those metals, which potentially mean taking gains and correction.

• China 45 iron ore ports arrivals at 28.47 million tons, up 7 million tons on the week. Six northern ports arrivals at 14.398 million tons of iron ore, up 1.879 million tonnes on the week.

• According to the port authorities of Pilbara, Hedland exported 49.6 million tons of iron ore in April, up 14.6% on the year.

SGX Iron Ore 62% Futures& Options Open Interest (May 21st)

• Futures 117,804,600 tons(Increase 2,602,900 tons)

• Options 141,549,700 tons(Increase 1,321,500 tons)

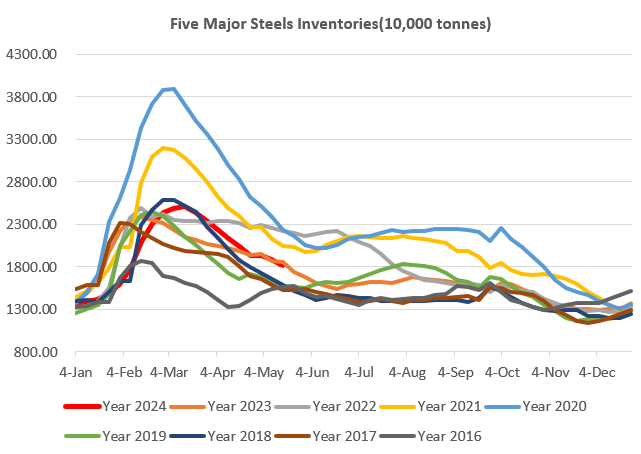

Steel Key Indicators:

• The HRC in Europe market was tepid in general, steel mills prefer to trade long-term in stead of spot cargoes. The North Europe HRC was traded around EUR660/t.

• China Zennith Group increased late May EXW rebar price by 50 yuan/ton to 3800 yuan/ton.

Coal Indicators:

• The Australia coking coal market inched up although eyeing a slow demand. The sellers were hard to give lower offers as most of cargoes were linked with June index. Indian buyers were covered till July.