Verdict:

• Short-run Neutral.

Macro:

• US Beige Book expected a mild growth recently on the consumer price.

• IMF raised its forecast for China’s projected economic growth to 5% from 4.6% in 2025.

• China State Council issued the Action Plan for Energy Conservation and Carbon Reduction from 2024 to 2025, which required that by 2024, the energy consumption and carbon emissions per unit of GDP be reduced by about 2.5% and 3.9% respectively, and the added value energy consumption of industrial units above designated size be reduced by about 3.5%. China will continue to implement crude steel production control in 2024, including the export of low value-added basic raw material products. By the end of 2025, the proportion of EAF steel production expected to increase to 15% over all steel making process, and the utilization of scrap steel expected to reach 300 million tons by then.

Iron Ore Key Indicators:

• Platts62 $118.75, +0.90, MTD $117.77. There were two NHGF traded at $116.55/mt and $116.6/mt respectively yesterday, and a PBF traded at $117.8. The mid-grade concentrates were traded more after a significant price drop. On the other side, buyers would evaporate once the price hike.

SGX Iron Ore 62% Futures& Options Open Interest (May 29th)

• Futures 133,587,300 tons(Increase 456,100 tons)

• Options 183,994,800 tons(Increase 927,500 tons)

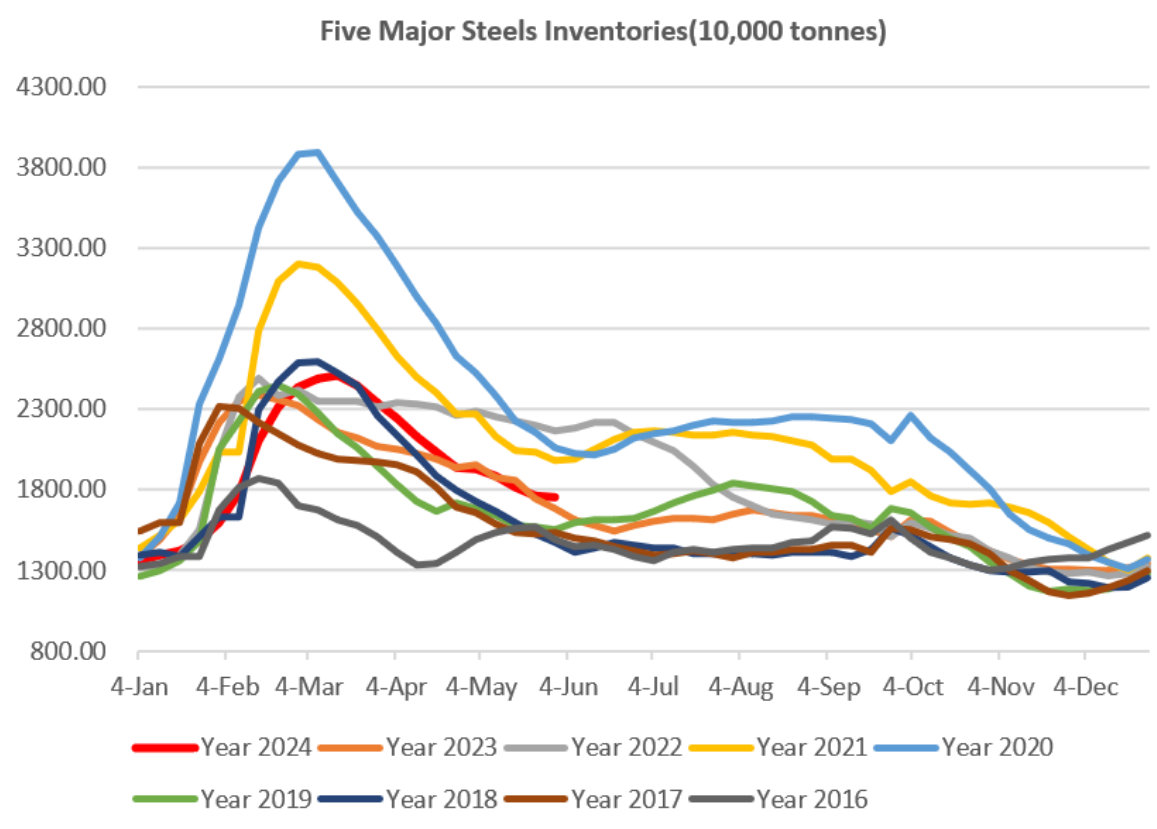

Steel Key Indicators:

• Indian currently imported Vietnam HRC at CFR $590-595/mt, imported China HRC at $570-575/mt. However China HRC lost competitiveness adding up tariffs.

Coal Indicators:

• The FOB market was lack of liquidity in general. The marginal market was led by Indian restocking as the concerning to use up import quota.