Market Verdict on Iron Ore:

• Neutral to bullish.

Macro

• Global June PMI 52.3, down 0.1 from May. U.S. PMI 56.1 down 3.1, lower than estimated 54.5. Euro Zone PMI 52.1, fell in estimation. U.K. PMI 52.8, refreshed new low from the June 2020. New emerging economies PMI 51.7, first time on mid point over last three months.

Iron Ore Key Indicators:

• Platts62 $109.90, -6.55, MTD $113.18. The physical July and August iron ore structure become contango since market participants believed that the bottom of the market was approaching. Chinese steel mills expect margin could recover with initiative control on production in June and July. Thus, Chinese blast furnace utilisation rate expected to drop in the coming few weeks. Silicon penalties in 4.5-6% range dropped from $4 to $3, suggesting mills tolerance on variety of brands, to comprehensively decrease the cost of materials. Seaborne float premium on PBF used to narrow 80% in the first two weeks of June, however this number become less volatile from $0.55-0.85 in late half of June with no actual trade on float basis. JMBF cargoes saw more trades at July Index with a $8.9 discount because the improvement on quality. Previously BHP narrowed term contract discounts for July JMBF from 11% to 9.25%, widened discount for MACF from 2.75% to 4%.

• China 45 ports iron ore arrivals at 65.63 million tons, down 1.5 million tons in June.

• MySteel estimated that total maintenance blast furnace has an impact of 103,300 tons of pig iron decrease during June 15 – July 4th.

SGX Iron Ore 62% Futures& Options Open Interest (Jul 1st)

• Futures 76,490,800 tons(Increase 657,200tons)

• Options 74,703,600 tons(Increase 1,036,900 tons)

Steel Key Indicators

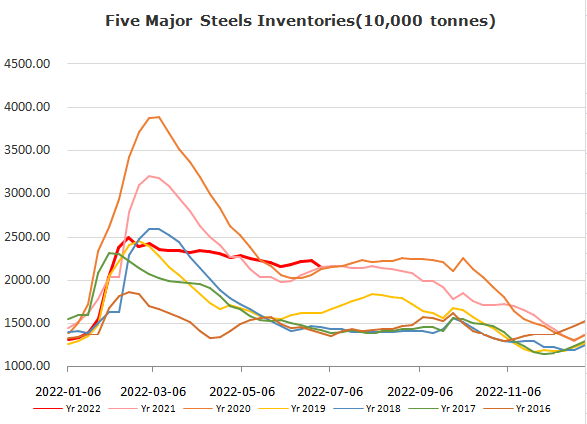

• Steelbank rebar inventory 7.26 million tons, down 3.62% w-o-w. HRC 3.21 million tons, up 1.08% w-o-w.

Coal Indicators

• Few Shanxi steel mills officially start the second round of coke price cut by 200 yuan/ton, after a previous delay by two and half weeks.