Market Verdict on Iron Ore:

· Neutral to bearish.

Macro

· China October CPI up 1.5% y-o-y, est. 1.3%, last 0.7%. China October PPI 13.5% y-o-y, est. 12%, last 107% y-o-y. U.S. PPI up 8.6% y-o-y, a ten-year-high.

· U.S. ADP statistics indicated jobs increased 571,000 in October, est. 400,000, which created the highest since this June.

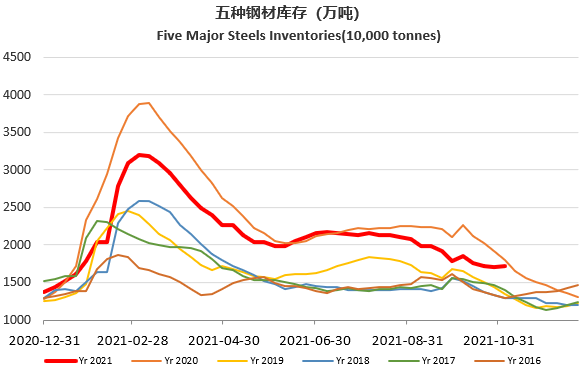

Iron Ore Key Indicators:

· Platts62 $92.45, -1.40, MTD $96.42. Iron ore futures and physical market both started a new round of big correction in early half of the week. Qingdao Port iron ore offered down 27 yuan at 630 yuan/tonne. December seaborne PBF was imported in a premium at $0.9, very low area in a trackable records. The low premium indicated mills have no preference among seaborne, ports inventories or physical traders’ resources. SGX Jan -Feb 22 contracts spread narrowed to $0.4-0.45, a historical low area, indicating the market was rather positive on the demand resilience after Chinese New Year next year, however still negative on the demand before the Chinese New Year.

SGX Iron Ore 62% Futures& Options Open Interest (Nov 9th)

· Futures 69,614,000 tonnes(Increase 1,191,100 tonnes)

· Options 64,269,500 tonnes(Increase 830,000 tonnes)

Steel Key Indicators

· Tangshan Qian’An billet down 300 yuan/tonne in Nov 8th and down 150 yuan/tonne in Nov 9th at 4450 yuan/tonne.

· China NDRC published a green production draft to encourage transmission from the high pollution industry to low carbon emission industry. Encourage steel industry transmission from blast furnace to EAFs.

Coal Indicators

· China Shanxi steel mills lower the coke price by 200 yuan/tonne, total down 600 yuan over the last three rounds.

· China railroad thermal coal transportation during October reached 157 million tonnes, up 26.8% w-o-w. The thermal coal at power plants inventories useable for 21.8 days, up 7.8 days from late September.