Verdict:

• Short-run Neutral.

Macro:

• US Labour department statistics indicated February CPI up 0.4% on the month, up 3.2% on the year, both fell into expectations. The strong CPI indicated a stubborn inflation condition, which decreased the probability to see interest cut before June.

• EIA increased daily oil production by 90,000 barrels/day, however decreased the global oil production because of the OPEC cut.

Iron Ore Key Indicators:

• Platts62 $110.30, +1.90, MTD $115.31. China mills cut and extension of maintenance resisted iron ore upside room. The short-run supply became crowded, while there was hardly chances to sell in secondary market. The stablisation on fundamental side needs to see a recovery on pig iron production as well as a destocking on ports.

SGX Iron Ore 62% Futures& Options Open Interest (Mar 12th)

• Futures 104,731,100 tons(Increase 499,400 tons)

• Options 113,063,600 tons(Increase 2,250,000 tons)

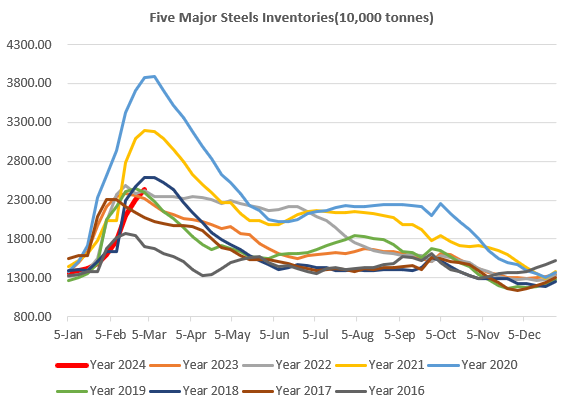

Steel Key Indicators:

• India JSW planned to start a blast furnace with 4.5 MPTA as early as 2026.

• Platts surveys across traders and end-users indicated that 86.7% participants predicted a down trend for US HRC delivered in March.

Coal Indicators:

• The FOB Australia coking coal maintained bearish as the lower bids on buyside. Both PMVs and PLVs were in similar trading range at $280 – 290/mt, obviously the correction shouldn’t be over at this level.

• China physical coke market down 100 – 110 yuan/ton recently, total down 500- 550 yuan/ton from January.