Market Verdict on Iron Ore:

• Neutral to bullish.

Macro:

• OPEC decreased the oil market demand for the fifth time in 2022 since April. The OPEC expected the oil demand in 2022 at 2.55 million barrels/day, down 100,000 barrels/day from last report.

• China Tianjin published 14 detailed practices to support automobile consumption. The industry expected to see more stimulus over the country currently.

Iron Ore Key Indicators:

• Platts62 $95.30, +3.05, MTD $87.73. Iron ore saw an uptick supported by both marginal ease expectation on epidemic control in China as well as solid measures to back housing market. However, seaborne buying interest maintained weak for two weeks, although the import loss almost disappeared. BHP sold a 90,000mt NHGF at $94.9/dmt for December laycan. Float basis NHGF premium around $1, PBF premium around similar level, both based on December Index. Both seaborne and portside liquidity were poor.

• Last week, 45 Chinese ports iron ore arrived 25.589 million tons, up 2.84 million tons on the week. 19 Australia and Brazil iron ore shipment at 23.587 million tons, down 2.662 million tons on the week.

SGX Iron Ore 62% Futures& Options Open Interest (Nov 14th)

• Futures 109,343,400 tons(Increase 3,250,000 tons)

• Options 84,034,500 tons(Increase 667,500 tons)

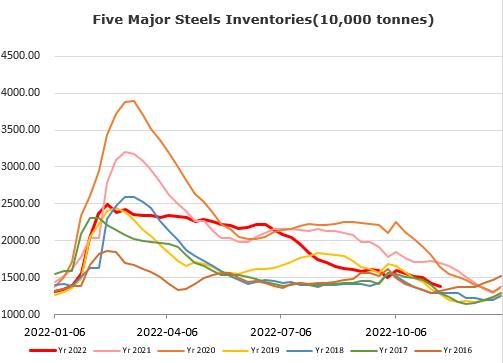

Steel Key Indicators:

• Mysteel researched 247 blast furnace operation rate at 77.21%, down 1.57% w-o-w. Utilisation rate 84.09%, down 2.23% w-o-w.

Coal Indicators:

• Chinese physical coke decreased three rounds total 300 -330 yuan/ton. Coke plants utilisation rate was in low area. Market participants believed it was difficult to see further cut on coke output.