Verdict:

• Short-run Neutral.

Macro:

• India steel maker Vedanta Sesa Goa subsidiary Wester Cluster Ltd announced to invest $2 billion dollars in Lybia to support its iron ore production.

Iron Ore Key Indicators:

• There was no Platts index due to Singapore holiday. Thus, the trade was quiet on ports and seaborne. Futures market rebound, as there was bottom hunting traders following each time of correction in June. In mid-run, the supply of Australia maintains high, together with a slow decreasing pig iron production, both becoming resisting factors for iron ore market. The crude steel production cut target in Fujian, China once supported steel growth and iron ore growth yesterday.

• During past week, Australia and Brazil total delivered 28.607 million tons of iron ore, up 2.67 million tons on the week. China 45 ports iron ore arrivals at 22.074 million tons, down 2.29 million tons on the week.

SGX Iron Ore 62% Futures& Options Open Interest (Jun 17th)

• Futures 120,935,200 tons(Increase 1,965,900 tons)

• Options 165,807,200 tons(Increase 473,500 tons)

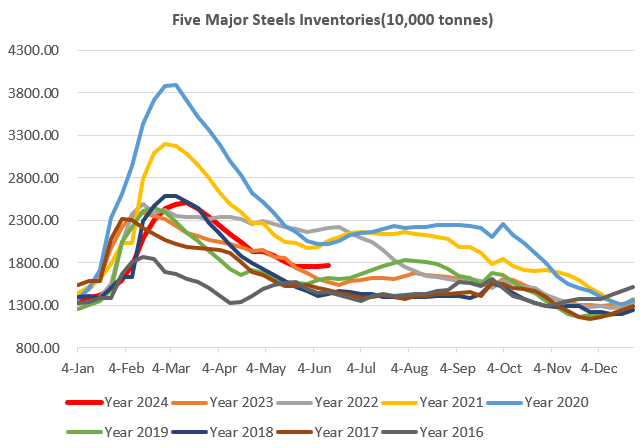

Steel Key Indicators:

• China 76 EAFs average cost at 3819 yaun/ton. Average production loss at 162 yuan/ton.

Coal Indicators:

• The trading sentiment on Mongolia coking coal was warming. There were a few trades at premium during past two days.