Market Verdict on Iron Ore:

• Neutral to bullish.

Macro:

• Euro Zone October CPI 10.6% on the year, est. 10.7%, refreshed historical high. CPI up 1.5% on the month. The food and energy price were still major contributors to support Euro Zone inflation.

• China automobile production 2.559 million units, up 8.6% on the year. Jan-Oct total produced 22.668 million units, up 8.1% on the year.

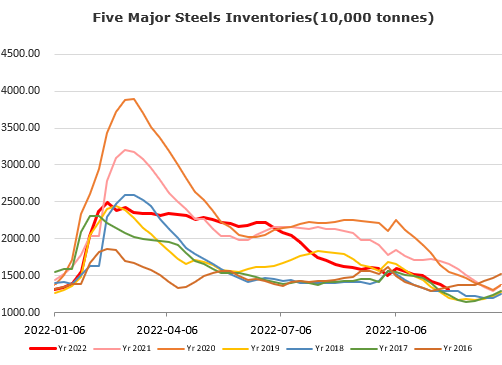

Iron Ore Key Indicators:

• Platts62 $98.35 (+0.25), MTD $89.95.Iron ore saw an uptick supported by both marginal ease expectation on epidemic control in China as well as solid measures to back housing market. However, seaborne buying interest maintained weak for two weeks, although the import loss almost disappeared. BHP sold a 90,000mt NHGF at $94.9/dmt for December laycan. Float basis NHGF premium around $1, PBF premium around similar level, both based on December Index. Both seaborne and portside liquidity were poor.

• MySteel sample mills iron ore inventories at 90.67 million tons, down 2.48 million tons on the week.

SGX Iron Ore 62% Futures& Options Open Interest (Nov17th)

• Futures 114,593,600 tons(Increase 2,277,300 tons)

• Options 88,243,200 tons(Increase 1,104,300 tons)

Steel Key Indicators:

• MySteel researched 414 sample steel mills in China, among which 65.2% steel mills indicated the negotiable range in steel price from 3200 -3500 yuan/ton.

• 40 EAFs in China average cost at 4035 yuan/ton, up 98 yuan/ton. Average profit – 68 yuan/ton.

Coal Indicators:

• Australia FOB coking coal index dropped by $28 during the week massively because of the crowded supply in December to January market. The most competitive offer was from Arcelor Mittal at $270 for 75,000mt Lawarra, the offer declined $10 from two days ago.