Market Verdict on Iron Ore:

• Neutral.

Macro:

• The new British Chancellor of the exchequer overturned Prime Minister Truss’s huge energy subsidy plan. Supported by the news, the British pound rose 1.54%, and the FTSE index was nearly 1% by closing.

• U.S. Industrial production growth rate increased 0.4% in September compared with the previous month, driven by the growth in durable goods and non durable goods. But the confidence index of American home builders fell for the 10th consecutive month in October. The divergence in the previous two statistics showed that the impact of the Federal Reserve’s interest rate increase policy has a different impact in different economic sectors.

Iron Ore Key Indicators:

• Platts62 $93.75, -2.40, MTD $95.86. The trade activities on seaborne market return to stable mode with positive mid-grade trades, including MACF, PBF and NMHG seeing this week. However BRBF and IOCJ would potentially correct compared to other discount ores or mid-grade because of the extreme low margin in Chinese mills. Lump market was quiet because the speculation following meeting and production curb called an end in October.

• The Transnet Union in South Africa came to an agreement with workers with 3 year increase on salaries. Thus, port and railroads expected to recover soon. Iron ore export expected to recover from Oct 19th. Iron ore export total decreased 560,000 tons from Oct 10-16th.

SGX Iron Ore 62% Futures& Options Open Interest (Oct 18th)

• Futures 96,604,100 tons(Increase 997,900tons)

• Options 83,702,400 tons(Increase 1,568,000 tons)

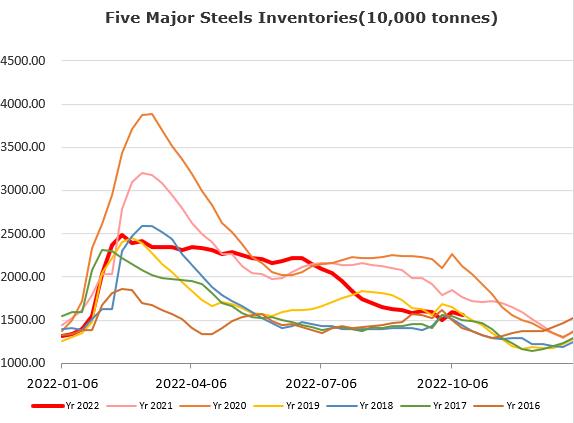

Steel Key Indicators:

• Tangshan lifted the sintering control in Tangshan from October 11-16th.

Coal Indicators:

• FOB Australia coking coal rebounded significantly yesterday by $7 to $293.5, concerning the supply tension. A deal was done at $288.25/mt FOB Australia for 30,000 mt of PLV Peak Downs with a Nov. 15–24 loading laycan. A bid was observed at $292 for 75,000mt GlobalBOAL HCCA Goonyella.