Verdict:

• Short-run Neutral.

Macro:

• US 10-Year-Bond yield reached 4.996%, the highest since July 2007.

• China NBS: From January to September, China produced 176.62 million tons of long steel, up 0.3% on the year. China produced 742.77 million tons of iron ore, up 6.1% on the year. China produced 36.83 million tons of coke, up 2.6% on the year. China produced 20.905 million automobiles, up 4.6% on the year. China produced 177,938 units of excavators, down 23.5% on the year.

Iron Ore Key Indicators:

• Platts62 $119.35, +1.00, MTD $118.56. In short-run, the low port stocks in China as well as low seaborne iron ore inventories in steel mills support the current resilience of index. Seaborne iron ore saw stable trades during the week, most of which were fixed price trade. However, market participants were worried about the resilience of the demand in November market.

SGX Iron Ore 62% Futures& Options Open Interest (Oct 19th)

• Futures 132,059,500 tons(Increase 2,390,200 tons)

• Options 116,635,100 tons(Increase 169,500 tons)

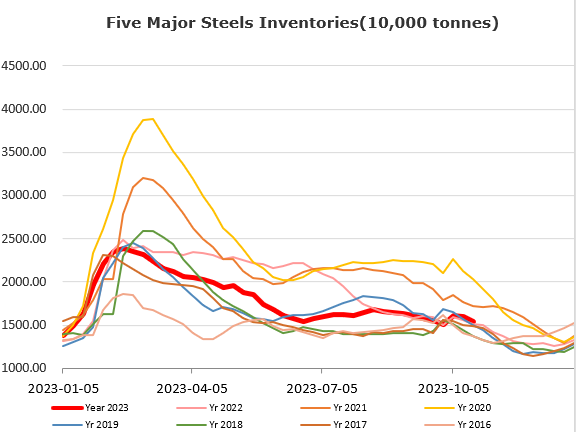

Steel Key Indicators:

• MySteel estimated 40 independent EAFs average cost 3894 yuan/ton, average loss at 133 yuan/ton.

• China NBS: China crude steel daily production reached 2.737 million tons, down 1.8%. Daily pig iron 2.3847 million tons, down 0.9% on the week.

Coal Indicators:

• The FOB Australia coking coal returned to a quiet mode after a sharp fall on Thursday. This week is Indian holiday, Indian buyers still have some buying interest for Nov/Dec PMVs. However, there was potentially reselling interest at lower levels following the low price on Thursday.