Verdict:

• Short-run Neutral.

Macro:

• The ECB regulator stated that the probability of 25bps or less interest cut in 2024 should be very low. It is currently difficult to predict the time of interest cut. The interest rate spread between the European Central Bank and the Federal Reserve may widen in future.

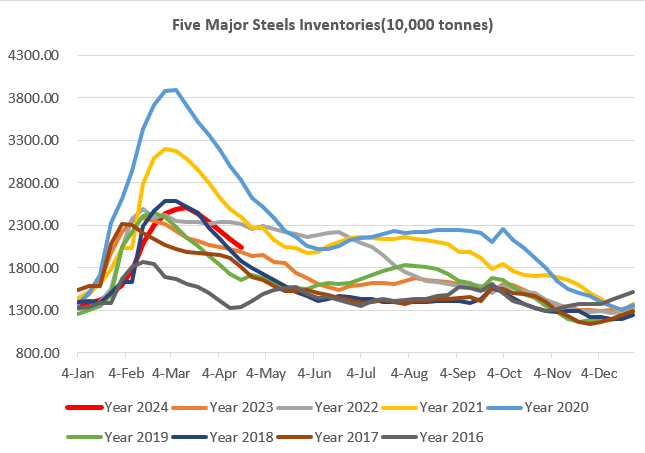

Iron Ore Key Indicators:

Platts62 $117.50, -0.30, MTD $107.77. Iron ore import in China above 100 million tons, up significantly from last year, however April shipment expected to maintain high level as well. The premium concentrates expected to slow down on procurement as unstable outlook on margin in long-run. Thus discount should be popular by comparison. The positive landing margin supported the seaborne iron ore in general. In short-run, the decreasing volume after a big growth indicated physical market was not buying the sentiment of sustainability.

SGX Iron Ore 62% Futures& Options Open Interest (Apr 19th)

• Futures 118,135,900 tons(Increase 466,000 tons)

• Options 136,047,900 tons(Increase 2,064,500 tons)

Steel Key Indicators:

• SS400 HRC FOB China up $10 to $525 last week with improving sentiment in Asia market. The uptick was also due to the mid-east tension which potentially raise the freight rates.

• Shagang Group increased rebar ex-factory price delivered in late April to 3970 yuan, up by 50 yuan.

Coal Indicators:

• In last week, China physical coke ended 8 rounds of correction and started to land first round of price increase, symbolised an entrance of ascending trajectory. The best FOB Australia coking coal bid was $254/mt last week.