Market Verdict on Iron Ore:

• Neutral.

Macro

• IMF decreased the U.S. economy growth rate from 3.7% to 2.9% in 2022, 2.3% to 1.7% in 2023.

• Global energy bureau predicted the investment in energy would increase 8% in 2022, equivalent to 2.4 trillion U.S. dollars, mainly contributed by green energy sources and power grid.

Iron Ore Key Indicators:

• Platts62 $115.00, -1.05, MTD $131.79. Float base iron ore premium dropped massively from $2.8 to $0.45 over the last ten trading days with no bids. Mainstream iron ores didn’t saw any active buyers during this week although improving import margins. The steel margin was suffering a loss. As expected, iron ore eroded steel mills margin and made an overdraft of growth in advance. Thus, mills are currently utilising premier coking coals to increase reducibility of low grade iron ore, which could reduce cost comprehensively. The 45% tax increase on Indian pellets and previous Ukraine supply disruption to Asian countries led to a global seaborne pellets shortage, which yet to see any alternative.

• BHP narrowed term contract discounts for July JMBF from 11% to 9.25%, widened discount for MACF from 2.75% to 4%.

SGX Iron Ore 62% Futures& Options Open Interest (Jun 24th)

• Futures 96,978,300 tons(Increase 1,846,100 tons)

• Options 89,022,500 tons(Increase 1,045,000 tons)

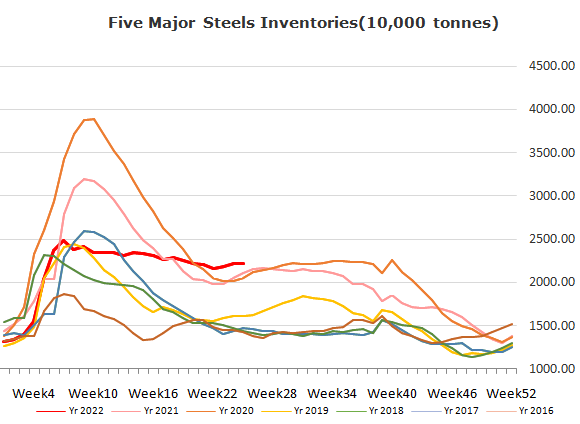

Steel Key Indicators

• 247 blast steel mills operation rate 81.92%, down 1.9% w-o-w, down 4.93% on the year.

• China 85 EAFs average operation rate 57.65%, down 3.11% w-o-w, down 25.36% on the year.

Coal Indicators

• The most competitive offer of FOB Australia offer was heard at $345/mt of HCCA Unbranded with July laycan. Met coal PLV plunged on strong selling interest because of the lackluster demand in China market.